HPHT Dividend: Respecting The Li Ka-Shing Faithfuls

I admire your loyalty to the Li Ka-Shing brand for the long-time investors who held Hutchison Port Holdings Trust (HPHT) from an IPO price of USD1.01. It sure wasn’t easy to watch the share price drift all the way down to USD 0.10 per share and struggling to hold on to the price when the world entered into some forms of pandemic lockdowns.

HPH Trust, like all the trusts (i.e. real estate, hospitality etc), is always a play on dividends. When it announced its interim dividend of HKD 0.065/unit against a nearly 4-fold increase in semi-annual earnings, investors are hesitant to trust the Trust – so to speak. The dividend is more than 50% increase from the last year’s interim dividend of HKD 0.043 / unit. Share price closed unchanged at USD0.225 apiece on 27 July 2021.

For all the negative reputation HPHT chalked up on its way down from USD 1.01/unit (i.e. trapping investors with dividends), I can understand the predicament investors face. Is this another dividend trap with an unsustainable 10% annual dividend yield? After all, it wasn’t so long ago that management retained investment interest with unsustainable dividends amid crushing leverage and poor earnings outlook. Finally, the dividends had to be depressed in reflecting its proper fundamentals.

With the latest 1H2021 report, is HPHT looking sharper on the earnings front to give sustainable dividends? I look for clues, whether management is pulling a cheap shot once again at newbies.

Three Key Takeaways From 1H 2021 Report Card

1) HPHT Is Benefitting From A Resurgent Container Shipping Sector

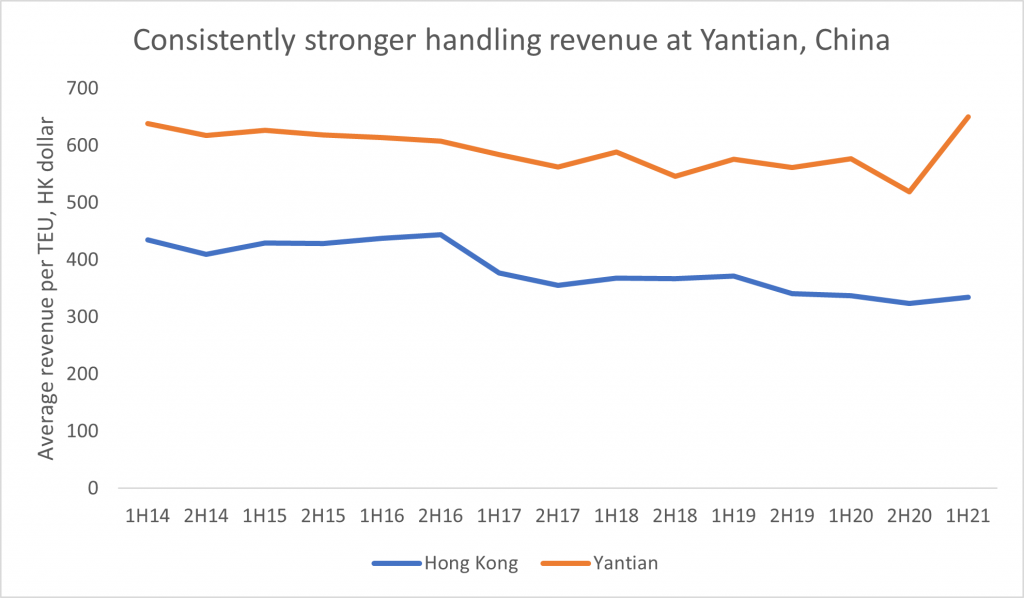

While the pandemic negatively impacted many businesses, container shipping businesses are recording one of the best years since the global financial crisis in 2009. The average revenue per container of HPHT rose 10.7% year on year in 1H 2021. Juxtaposing with the sea freight cost per container to the key EU and US markets, which jumped at least 300% from early 2020, it is not inconceivable that the container terminal operators like HPHT would open negotiation with shipping lines for a higher handling tariff.

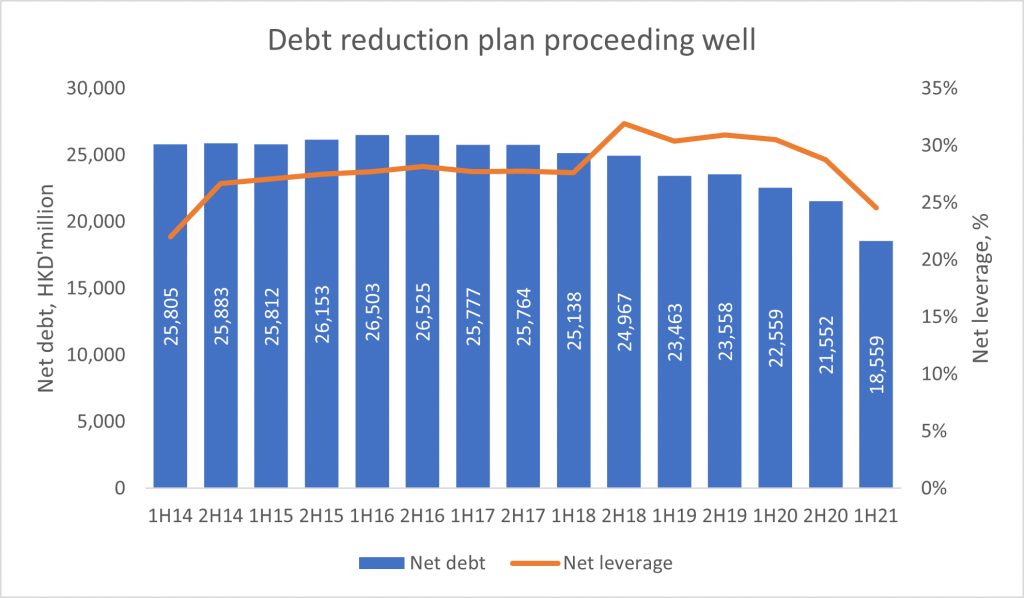

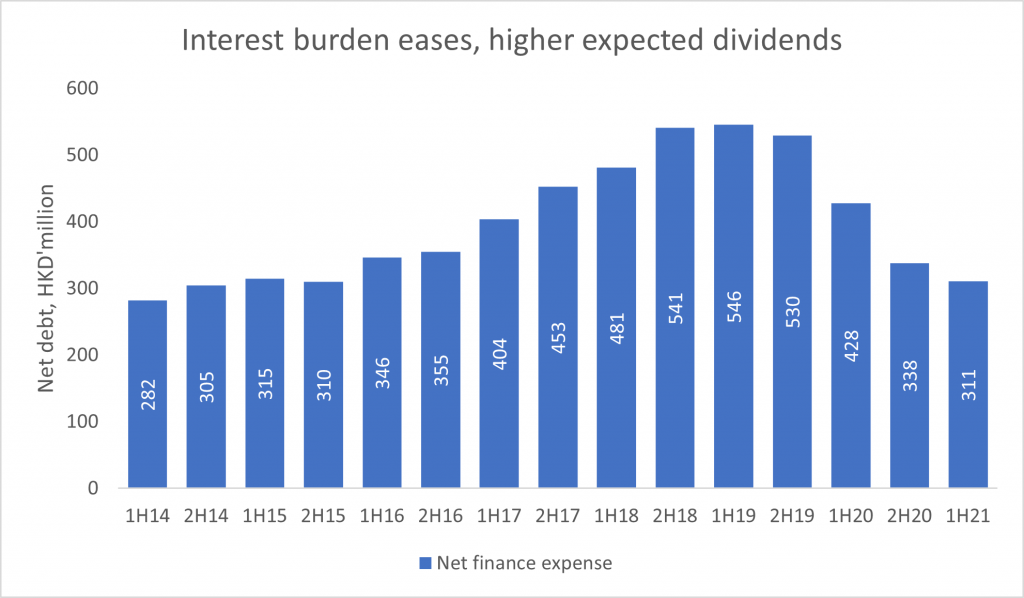

2) Continual Reduction In Leverage To Save Interest Cost

Since 2018, HPHT is diligently paring its debt. Net debt of the Trust fell from HKD 25.9bn in 2014 to HKD 18.6bn in 1H 2021. The semi-annual net interest expense of HKD 310.9 million in 1H2021 was the lowest in 6 years. As the interest burden eases, management could distribute more of its operating profits. Barring exceptional CAPEX from the expansion of Yantian East Port, the continuous reduction in leverage bodes well for a stronger dividend payout.

3) Pivoting To Mainland China, Valuation Upside For A Bumper Dividend

The port casuals would think of HPHT as a play on Hong Kong. What is little known is the fact that the port at Shenzhen Yantian (mainland China) is expanding rapidly, generating about two-thirds of the Trust’s revenue. The state-owned enterprise Cosco Shipping Ports tied up with HPHT to co-manage their berths in Hong Kong, effectively a merger of the sort. Furthermore, both companies have set up a joint venture to expand Yantian East Port. With the assertion of power by the central government in Beijing on Hong Kong, we can’t rule out an acquisition of HPHT, the priced trade-enabling infrastructure asset in the Pearl of the Orient (东方之珠).

There is spare port capacity in Hong Kong, presenting a monetisation option for management if debt is to be pared as soon as possible. Average box revenue at Yantian is almost double that at Hong Kong. As the average handling revenue continues its descent, it makes sense for management to encash the remaining lease on the port premise, possibly to a Chinese port operator. Should an acquisition happen, we can look forward to a special dividend.

In A Nutshell: HPHT

These 3 key reasons are why I believe the dividends are sustainable, at least for as long as the pandemic last. In about 6 months, HPHT will report its full-year 2021 results and probably a corresponding final dividend. If the 51.7% interim dividend hike is of any reference, we could potentially be looking at HKD 0.117 /unit for the final dividend. It should nicely translate into a full-year dividend yield of 10.4% (FX rate of HKD0.1287/USD against the share price of USD 0.225/unit). Respectable, in my opinion, when most trusts on SGX are already trading above their pre-pandemic levels without not much dividend to back their moats.

Technical Consolidation Near Support

HPHT bottomed out when the pandemic became evident with the US and Europe entering lockdowns in the second quarter of 2020. Just as the share price was recovering from the all-time lows, the passing of the security laws that curtailed the political freedom in Hong Kong slammed it below USD 0.10/unit. Technical rebound was intact, supported by macro tailwinds from the shipping cycle recovery.

In the past 2 months, HPHT is consolidating in the range of USD 0.21/unit and USD 0.245/unit. Traders were unfazed by the positive earnings, unless the share price moves into the uptrend bracket at a minimum USD 0.275/unit. Meanwhile, even in the sideway movement, the current share price is positioning nicely near the support level of USD 0.21/unit. When the Trust goes Ex-Dividend, the theoretical share price would be USD 0.215, which is still supported by the volume-driven technical trends.

About The Contributor

Victor was an investment analyst with a global consulting firm based in the UK. In 2017, he was ranked on Bloomberg as the top analyst in his equity coverage of stocks in excess of USD 20bn. His area of interest is in stocks that were once darlings of aunties and uncles, but still have a fundamental story to tell. These unloved stocks generate some of the best returns because they move up quietly without excessive coverage by brokerage houses. Below is a sample of his “lovers” made known on Collin Seow’s blog.

Note: Capital return based on prices obtained on 27 July 2021

If you’d like to learn more about systematic trading to better time your trade entries, click the banner below: