SATS Stock Singapore: Should You Buy Sats Shares Now?

SATS Ltd, one of the leaders in the aviation airline catering (and the one responsible for flight meals on SIA Group of airlines) market, is constantly looking to refine the art of serving in-flight meals, with the aim to possibly rival Michelin stars restaurant perhaps?

While I might not be a huge fan of airline food (neither am I a huge fan of SIA – well the company has been voted in a 2019 employee survey as the best company in SG to work for – must be the SQ lady perk), SATS is undoubtedly a company that has been on my investment portfolio radar screen for a while. What do I like about the company?

3 Key Points To Rule:

#1 Positive Macro Trend

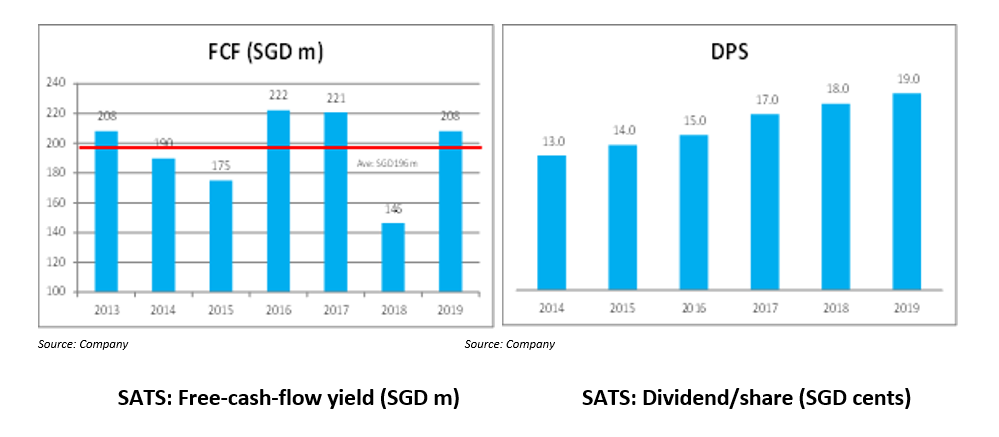

Air travel is rising and this is a trend that will rise for decades to come. More passengers = more aircraft = more meals = more $$$ for service providers. SATS is a natural beneficiary of the growing proliferation of air travel and one with a low maintenance capex nature (unlike airports that generally have to fund huge spending for terminal expansion). SATS spends approx. SGD80-90m per annum in capex relative to the SGD300m in operating cash flow, translating to a free cash flow of SGD200m/annum and rising that has been used to support dividend payments. In fact, SATS is one of the rare gems in the Singapore context that still pays an ever increasing dividend/share over the past 5 years.

#2 Consolidating Market Leading Position

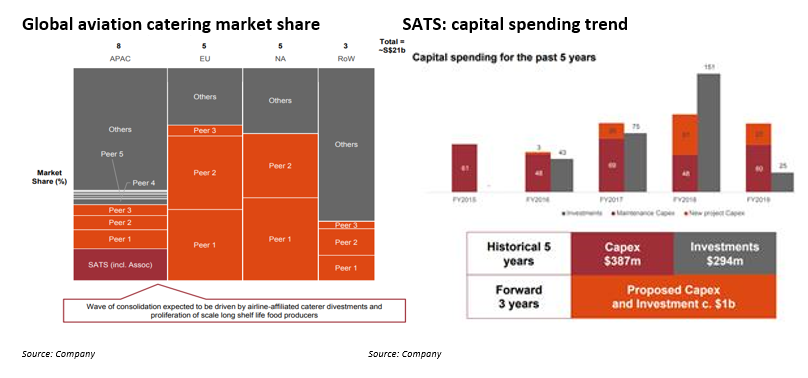

Already a market leader in SG and Asia Pacific, SATS is aggressively looking at opportunities to further expand its market share of the aviation catering market as well as ground handling market in this region (APAC is the fastest growing region in the world, in terms of aviation catering and ground handling).

In the company’s recently concluded Capital Markets Day (powerpoint slides can be downloaded from SGX), management highlighted the opportunities of them further increasing their market share dominance in this region due to airline-affiliated caterer divesting these entities to focus on their core passenger business.

In fact, management is so confident of the company’s current strategy that has taken them c.5 years to refine, that they are now going out with a bang è leveraging on its pristine balance sheet (net cash) to increase its investment momentum.

The company targets SGD1bn in new investments over the next 3 years vs. SGD680m done over the past 5 years. Imagine the earnings accretion if each investment yields an immediate 8% ROIC on purchase.

#3 Diversification

According to SATS, the company is looking to build up a strong network of central kitchen and food factory facilities in China and India to target the Fast Casual Restaurants (FCRs) – think the likes of Starbucks, Haidilao, Yum! China that owns KFC, all of which are existing customers of SATS.

It makes perfect sense to us why the company is targeting this non-aviation segment (and seemingly losing focus on maintaining its aviation dominance).

To serve the fast growing China aviation market, you need an efficient aviation food processing network which entails having central kitchens. These kitchens need not be exclusive to the aviation market and SKUs developed can often be sold to FCRs as well.

Hence by leveraging on already existing assets originally catered towards its core aviation business, SATS can now achieve diversification through the fast-growing FCR market.

About SATS Ltd.

SATS Management

It is always comforting to know that a good business is run by a good management. Warren Buffett once famously said that a good business is one “your idiot nephew” could run.

Over the past 10-years, according to management, SATS generated total shareholder returns of 472% (dividends plus capital appreciation), rivalled by only one other company in the STI index (Which one you might ask? Well that’s another read for another day).

SATS in today’s context is definitely not run by a bunch of fools (well one day it might, who is to say never) but with a business that is almost a monopoly in Singapore (80% of market share) and one with an ever growing business presence in APAC through multiple JVs, it is hard to ignore this business that is a natural beneficiary of one of the clearest macro tailwinds in the coming 2 decades.

SATS Share Price: Good Things Ain’t Cheap

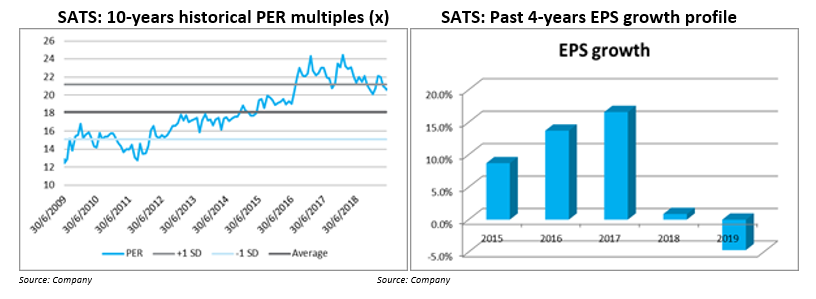

The reason why the counter is still in my radar and not already in my portfolio is due to its hefty valuation. (You can’t be generating 472% return and still look cheap, can you?)

My main grouse has been its premium valuation, trading at a hefty 21x forward PER while the past 2-years historical earnings growth profile has been less than A-star. Much less.

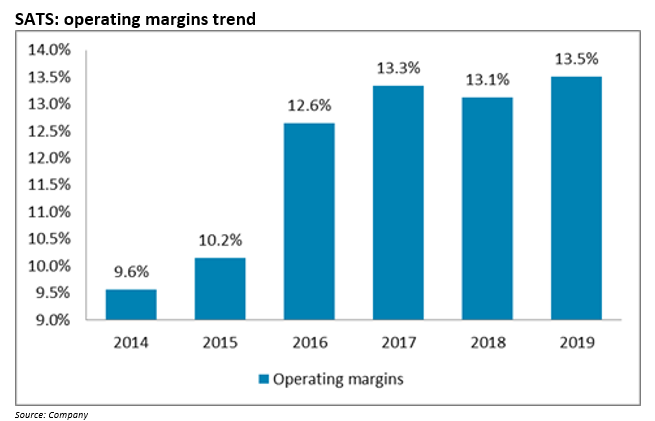

However this could all change with the company’s new growth strategy in place, one which entails accelerating its M&A profile to grow top-line (SGD1bn spending!!! Take my MARNEY) while keeping operating costs in check (check out the impressive growth in operating margins below).

Replacing the need for additional manpower with automation, robots, AI, digital platforms are just some of the “new-age” tools SATS engage to stay at the forefront of the current technological revolution, elevating its productivity and efficiency to be ever so relevant in a fast-changing world.

With Terminal 5 set for opening in 2025 that will almost double existing terminal capacity at Changi, businesses that can capitalise on this huge growth opportunity while ensuring optimal cost control will be the long-term winner.

And I believe that SATS has the in-built DNA to be one, regardless of the captain of the ship.

Conclusion: SATS Buy Or Sell?

Well after all that has been said. Is there a buying opportunity?

There is always an investment case for SATS and given my view of the company’s long-term rosy fundamental outlook, this is one that I am confident will sit well in your core (investment, and possibly trading) portfolio for the long-term.

If most of the stars are well-aligned, you get a company that can demonstrate double-digit EPS CAGR over 3-5 years horizon and get paid a yield of 3.5-4% as you wait for your fruits to ripen.

On a technical basis, I would be waiting for the counter to dip to a support level of SGD4.50 before making a purchase. You can see from our proprietary charts below that SATS does well on a broad basis when it’s in a bullish phase (blue candles). Which is right now.

No-telling if dropping to SGD4.50 would ever happen but with Trump being in the “driver seat”, I would bet that the chance of a significant market correction is more than even and SATS might well is the unwitting collateral damage, like so many “opportunities”.