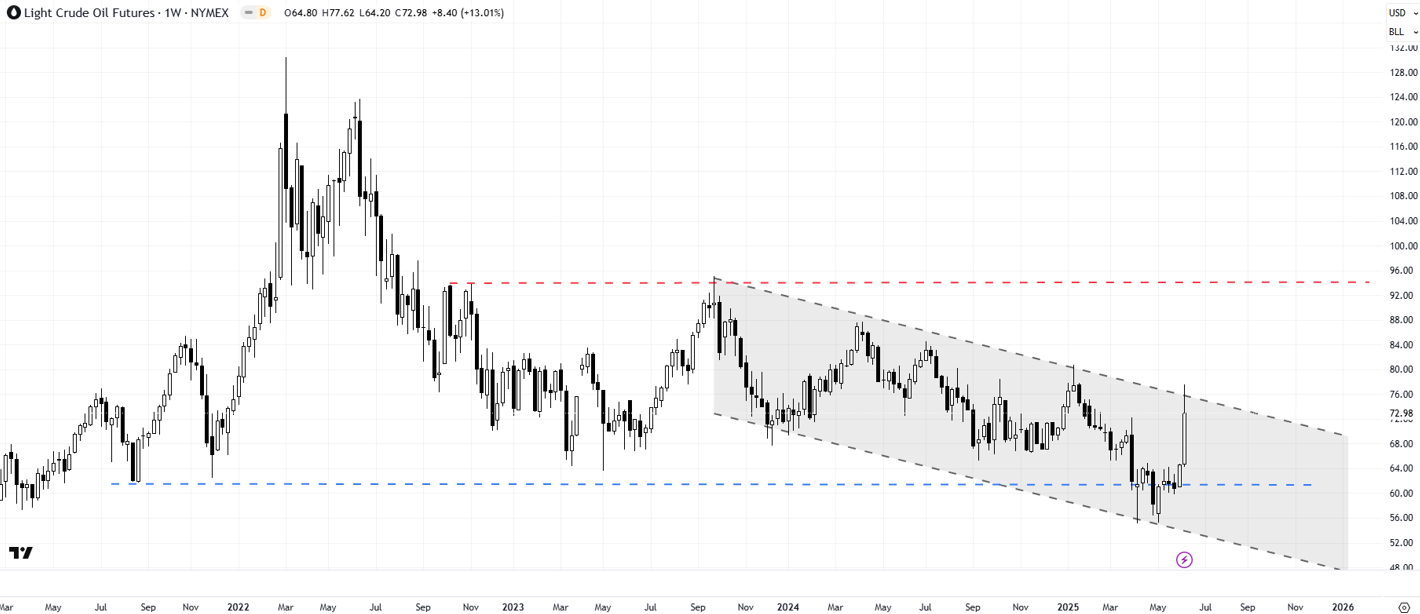

Within a span of two months, risk aversion has spiked once again after Israel launched military strikes on Iran last week.

Crude oil prices witnessed the biggest one-day rise since 2022 on fears of supply disruptions, safe-haven bids pushed gold higher, currencies of oil-exporters including Norway and Canada jumped, while the S&P 500 index declined.

Just two months ago, equity markets suffered the worst selloff since 2022, after US President Donald Trump’s announcement of reciprocal tariffs in April. However, risk sentiment has improved as trade tensions have eased after the US-UK trade agreement, US and China inch closer toward a trade deal, and potential trade resolution of US with its other trading partners. US President Donald Trump said on Sunday that the US has trade deals completed as he left for the G7 summit in Canada.

Crude Oil Futures (Weekly):

Following Israel’s strike, Iran retaliated with missiles, increasing the severity of the conflict. At the time of writing, Israel has vowed to intensify its operation, according to media reports. United, Delta, Turkish Airlines and a number of other carriers have reportedly cancelled Israel flights or extended a suspension of service.

The hope is that Israel-Iran conflict doesn’t turn out to be a protracted one and remains contained, especially with regards to energy and other supplies, including fertilizers. A prolonged period of uncertainty could pose a setback to business and investor sentiment, weighing on global growth. Despite easing trade tensions, the outlook on global growth remains gloomy due to US tariffs. JPMorgan CEO Jamie Dimon has warned that the US economy could start to deteriorate soon.

In the short term, equity markets are likely to remain under pressure, especially if the conflict intensifies. Already, equity markets were looking a bit overbought and showing signs of fatigues given the sharp rally in recent weeks. Geopolitical tensions provided an excuse for some to take some cash of the table.

S&P 500 Index (Weekly):

On technical charts, the S&P 500 index faces stiff resistance at the record high of 6147 hit in early 2025. There is immediate support at the late-May low of 5765. Any break below would be a signal that the short-term upward pressure had eased. Subsequent support is around 5500. The longer-term outlook is unlike to be at risk while the index remains above strong support on the 200-week moving average (now at about 4750).

If history is any guide, in the short term, there is a hit to sentiment as markets try to grasp the severity, length and breadth of such events. However, following a period of war or terrorist attacks, more often than not, markets do tend to recover in subsequent months. For long-term investors it might make sense to stay the course and ride out the volatility. If the decline in equities turns out to be deeper, it could provide an opportunity for those on the sidelines or who missed the quick rebound in recent weeks.