Market has been on a bullish run since the world breathed news of Pfizer’s COVID19 vaccine with an efficacy of more than 90%. Market crept higher on Moderna news that its vaccine is slightly better than Pfizer’s. While we are feeling optimistic about a resumption of the normal that we were used to, I believe most of us can’t help but feel pity that perhaps we had missed the lows in March 2020 and early November 2020. Should we ride the upswing as charting indicators seem to suggest or should we build some defense in our portfolio?

This is the TradersGPS daily chart of Moderna. It has been moving up ever since CoVid came into focus and TradersGPS system was able to capture a massive 180% first leg up and then a quick 30% on the recent vaccine news.

This is the TradersGPS daily chart of Moderna. It has been moving up ever since CoVid came into focus and TradersGPS system was able to capture a massive 180% first leg up and then a quick 30% on the recent vaccine news.

Here is the TradersGPS weekly chart of Pfizer, it’s been generally range bound for a number of years, not the ideal candidate for trend trading.

Here is the TradersGPS weekly chart of Pfizer, it’s been generally range bound for a number of years, not the ideal candidate for trend trading.

I would say build a portfolio with some allocation to companies you are perfectly comfortable to hold in a downturn yet continue to give out some dividends. Food and beverage sector is easy to understand, especially a debt-free F&B company.

Picture a mainly food (MF) business that sells and records fast-moving food products to consumer as revenue. Ingredients and food preparation cost, salaries of service staff, shop space tenancy form the business cash expense. Generally, revenue less such cash expenses would lead to the derivation of the operating cash flow.

If the MF company does not intend to invest too heavily in expansion, the bulk of the operating cash to available cash for dividend distribution. As a shareholder, it is always nice to have dividends in a bearish market, and capital gains in a bullish market. However, most of these stable MF companies are also boring and unloved with limited daily trading liquidity.

Just 3 criteria to get us going:

First, I like domestic companies that I can have a gut-sense on the business.

Second, I build my defensive position with net-cash companies that continue to bank in cash every quarter.

Third, with a layman perspective, I want to buy at a bargain in that the companies have to be price chart-wise cheap in recent history.

My MF list is not exhaustive but here are some that fit the criteria. It should not be taken as a recommendation to buy but solely sharing my perspective on what makes a fundamentally-sound and defensive stock.

If you have some spare travel cash not spent this year, and can live with low trading volume counters, ladies and gentlemen, be introduced to Old Chang Kee, Japan Foods and Kimly.

You would have seen these MF businesses every day, if not every week in your neighbourhood.

Old Chang Kee provided catering services to foreign workers in community care facilities, which partially offset the revenue weakness at their retail mall outlets.

This is the TradersGPS weekly chart of Old Chang Kee. Prices haven’t recovered to pre-covid levels, so there is some decent upside when society return to more normal levels of consumption.

This is the TradersGPS weekly chart of Old Chang Kee. Prices haven’t recovered to pre-covid levels, so there is some decent upside when society return to more normal levels of consumption.

The first criterion is essentially revenue exposure.

Thankfully, Singapore is one of the very few countries in the world with single-digit new COVID19 cases daily. Europe, Japan, South Korea, United States are experience third or fourth wave of the pandemic.

On the contrary, let us appreciate that Singapore is prudently easing COVID19 restrictions and that the government has been supportive of businesses.

The 3 “mainly food” companies, which predominantly serve Singapore market, shall see a resumption of revenue to pre-COVID19 levels faster than the other international companies.

This is the TradersGPS weekly chart of Kimly. Prices appear to have found a bottom with the massive market drop in March. It has since moved beyond pre-covid price levels in a sign of strength.

This is the TradersGPS weekly chart of Kimly. Prices appear to have found a bottom with the massive market drop in March. It has since moved beyond pre-covid price levels in a sign of strength.

The second criterion on cash position is an important consideration.

The whole defensive concept would fall apart if these MF stocks do not have positive cash flow to dish out dividends. The table below shows the latest financial positions filed with the SGX. Kimly and Japan Foods are likely to report their 1H 2021 earnings in a few weeks’ time.

| Old Chang Kee | Kimly | Japan Foods | |

| Latest results ended | 30 Sept 2020 | 30 Jun 2020 | 31 Mar 2020 |

| Cash | 25.3 | 76.4 | 20.4 |

| Debt | 7.3 | 4.4 | 0.0 |

| Net cash | 18 | 72.0 | 20.4 |

| Operating cash flow before working capital changes | 15.0 | 45.6 | 12.1 |

| Investing cash flow | -0.1 | -4.5 | -1.9 |

| Free cash flow | 14.9 | 41.1 | 10.2 |

| Annual free cash flow | 29.8 | 82.2 | 20.4 |

| P/E (TTM) | 21.5 | 23.2 | 57.0 |

| P/B | 2.5 | 3.8 | 1.8 |

| P/FCF (TTM) | 3.3 | 9.0 | 3.0 |

Evidently, all the 3 MF companies have the financial capacity to distribute dividends to shareholders. And they have continued to dish out dividends in these tough times. Japan Foods yields 2.9%, Old Chang Kee at 1.5% and Koufu at 3%. The dividends may be humble, but these are the rates the companies are comfortable to part their cash at.

This is the TradersGPS weekly chart of Japan Foods. Price has plateaued since the massive market drop in March this year.

This is the TradersGPS weekly chart of Japan Foods. Price has plateaued since the massive market drop in March this year.

The third criterion must be price point. Everyone in Singapore loves a good bargain. Even in a company that has solid fundamentals but has seen its share price ran up might draw some concern from you that it looks toppish for a correction. Good for us, these three “mainly food” companies have not run up that much compared to the Straits Times Index.

Source: POEMS, as of 17 Nov 2020

Source: POEMS, as of 17 Nov 2020

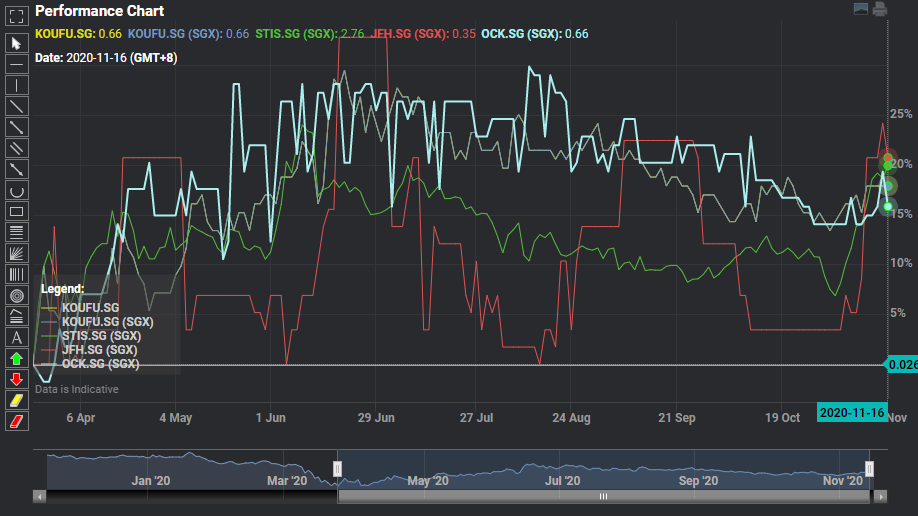

We take the view that 23 March 2020 was the lowest market price of 2020. Since then, STI has risen ca 20%, while Old Chang Kee and Koufu tallied about 16% gains.

With Phase 3 reopening of the economy, and possibly a resumption to the normal we were used to, we are looking at their share prices about 20-30% off their peaks. An uncomfortable question we might have to deal with is, what if the vaccines come up short, just like the Oxford vaccine? I guess the market would crash. However, I can be confident that their cash coffee should be enough to tide through a couple more years of COVID19 lockdowns.

This article was written by Victor, a veteran analyst who consistently ranked top 3 on Bloomberg within his niche, seaport infrastructure. He is a firm believer of a hybrid investment approach with both technical and fundamental knowledge.

If you’d like to learn more about systematic trading to better time your trade entries, click the banner below