Sell Singapore Banks To Buy Keppel?

Two significant news hit the headlines today.

SG Banks Dividends Cap

One: The Monetary Authority of Singapore (MAS) has called on locally-incorporated banks to cap their total dividends per share (DPS) for FY2020 at 60% of FY2019’s DPS and offer shareholders the option of receiving the dividends to be paid for FY2020 in scrip in lieu of cash.

MAS highlighted that while the local banks’ capital positions are strong, the dividend restrictions are a preemptive measure to bolster their resilience and capacity to support lending to businesses and individuals through an uncertain period ahead for our economy.

The news immediately took the wind out of our local banks, with their share prices falling between 3-3.8%. The general consensus on the street has been that both DBS and OCBC will likely be able to maintain their DPS payment for FY2020 while UOB will likely see a minor reduction. Hence, the MAS announcement definitely came as a negative shock.

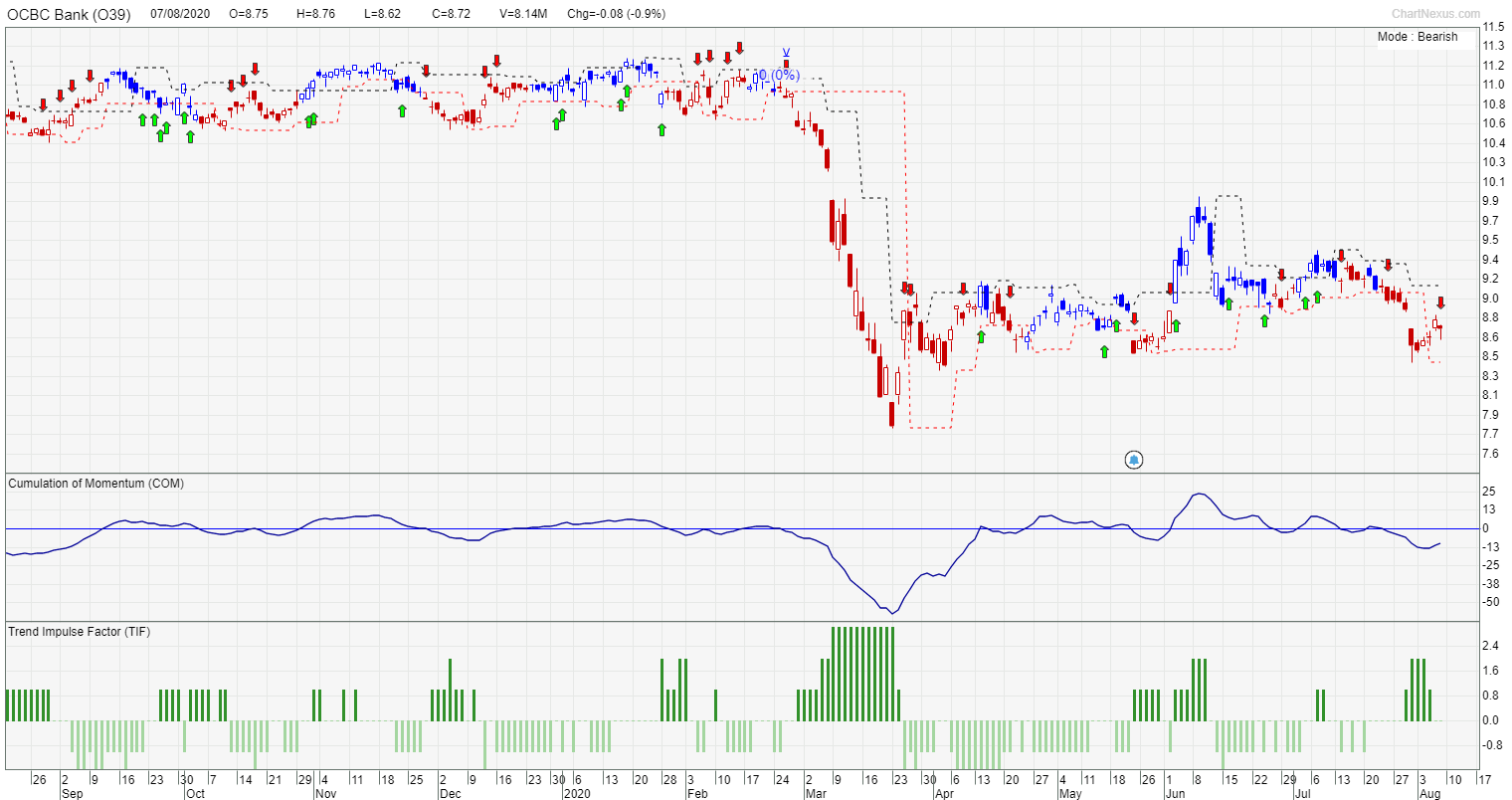

From this TradersGPS chart, you can see that OCBC tends to move in tight ranges, the only large trend was the dip in March this year.

Our local banks’ dividend payments have been viewed as “rock solid” and many investors continue to remain vested due to the fact that they will not be cutting dividends this year and the banks’ high dividend yields are considered an important factor of their investment thesis when it comes to owning banks in a recessionary scenario.

In recessions or the early-stage of an economic down-cycle, banks tend to be the hardest hit and it generally doesn’t make sense to be vested in banks, unless you have an extremely long-term view, like Berkshire Hathaway who continues to increase their stakes in Bank of America.

A high and possibly sustained dividend yield is typically one of the major considerations for investors to be holding to remain vested in banks under the current climate. According to Citi and UBS analysts, they believe that DBS might be the hardest hit due to the dividend restrictions, as the bank is seen as a bigger proxy for generating dividend income than its peers.

To be honest, I believe that our bank’s capital ratios, typically measured by their Common Equity Tier 1 (CET1) ratios, are likely the highest among the ASEAN banks, possibly alleviating concerns over a drastic erosion of their capital structure even in the worst-case scenario. Not concern that a “bank run” will happen in Singapore.

However, while investors and possibly many financial bloggers continue to hold faith in our local banks, I don’t foresee any sustainable catalyst over the horizon (now that their yields are no longer as juicy) to propel their share price higher in today’s context. While we might see “one-off black-swan” trading related gains in their 2Q20 announcement, just like what the US banks had announced, this is unlikely to be sustainable heading into 2H20.

Piyush Gupta, the CEO of DBS, said in an interview with CNBC in the middle of this month, that banks could experience “far more damage” to their balance sheets when stimulus measures that are keeping many businesses afloat are rolled back. He highlighted that governments cannot keep supporting the business community financially, so defaults will start rolling in sooner or later which will spill over to the financial sector.

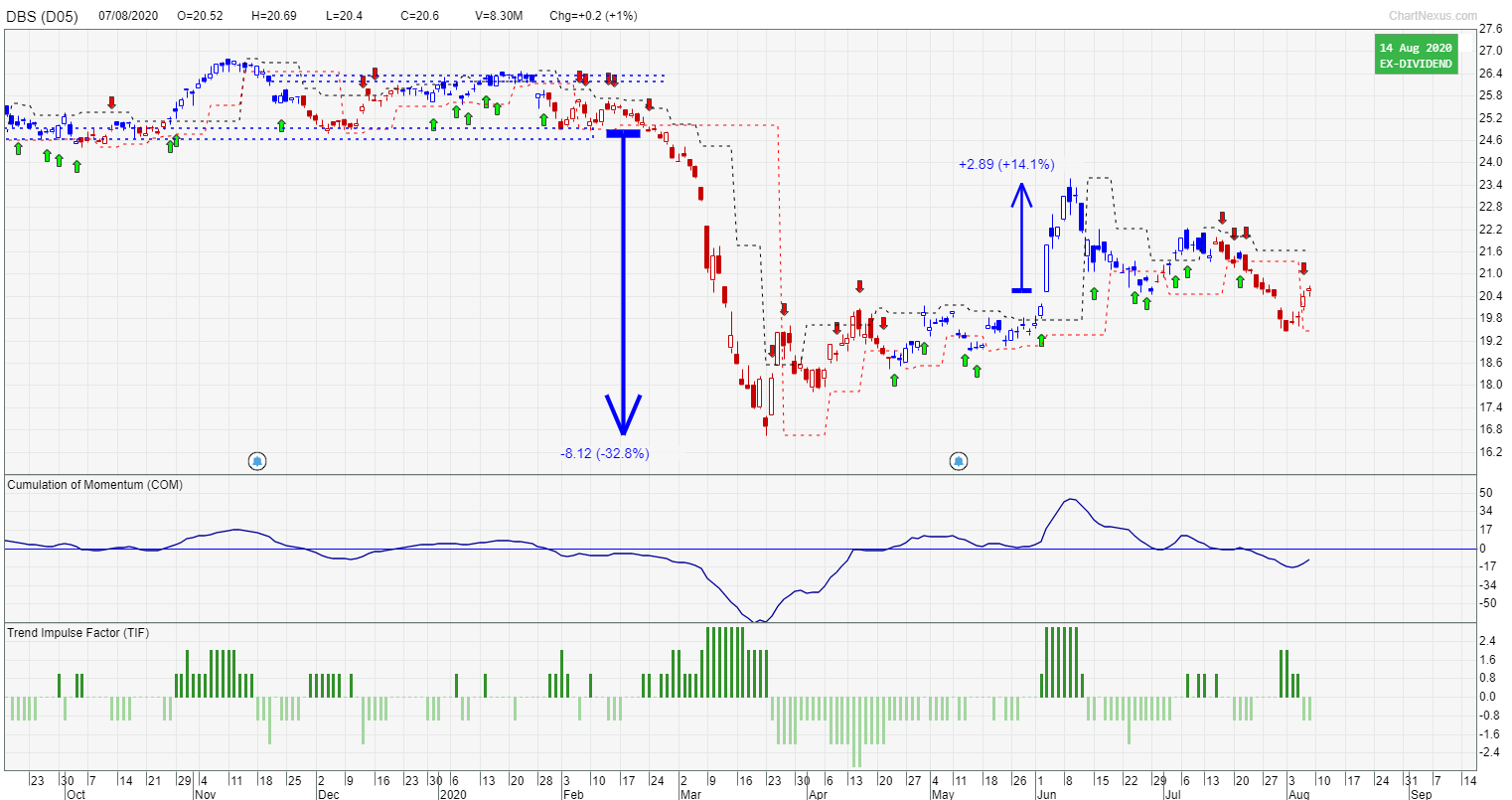

From this TradersGPS chart, you can see that by following the system, there were signals to capture the huge 30% sell off in March, and subsequently a buy signal that saw up to 14% profit in a few days.

He thinks the challenge is not in 2020 but the real pain will be felt in 2021. While he did not suggest that a voluntary dividend cut would be imminent in that interview, he highlighted the possibility of that if the economic outlook turns out to be grimmer than their expectations.

Well, MAS has done that “hard work” for him.

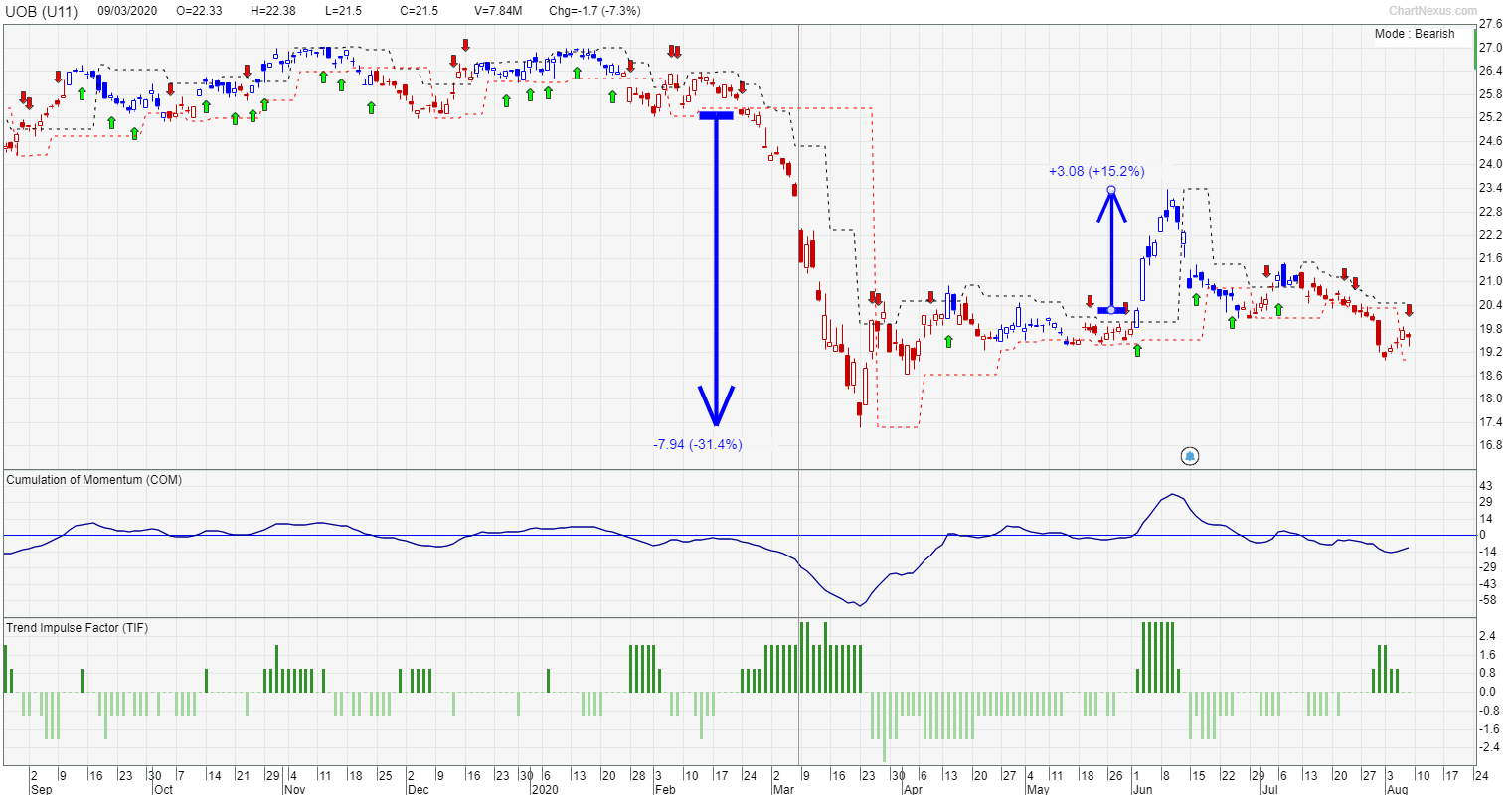

This TradersGPS chart shows the sell signals would have caught the 30% drop in March for UOB, and more recently a buy signal that showed almost 15% gains over a few days.

At the end of the day, banks are still a necessity, for now. We are seeing increasing options from fintech companies offering compelling financial products for us to park money with them. However, they are not yet at the stage where they can provide a combination of trust and scale for consumers.

NOT YET are the keywords here as we are already seeing banking licenses possibly being issued to these fintech companies. Once fintech companies established the trust and scale required to win over consumers totally, we might see the end of days for banks.

All said and done, I believe that investing in our local banks is the “safe route” but not necessarily the right one unless you have a really long enough time horizon. That however, is usually what investors “convince” themselves when their investments head the wrong way. Stay long term guys!

Keppel Disastrous 2Q20 Results

The second big news is Keppel announcing a disastrous set of 2Q20 results, with a reported net loss of S$698m for the quarter. As a result, they have failed to meet a pre-condition for Temasek takeover bid. Loh Chin Hua, CEO of Keppel said the following:

“We believe that the 20% threshold in the MAC (material adverse change) clause in respect of net profit after tax has been crossed, which means that the MAC pre-condition in Temasek’s pre-conditional offer has not been satisfied”.

Nonetheless, the deal has a long stop date of Oct 21, meaning that Keppel could make up any shortfall in its 3Q20 results. Alternatively Temasek also has the right to waive its pre-conditions.

Analysts in general forecasted potential impairments losses of around S$150m for the quarter. Keppel surprised with a massive S$919m impairment for 2Q20 as shown in the table below.

While Keppel has provided a profit guidance a few days back (resulting in a c.4% drop in its share price after the announcement), the magnitude of these impairments likely took the market by surprise.

Whether this is a kitchen sinking exercise, a one-off for this quarter or a prelude to more pain in its O&M division remains to be seen.

However, it is clear for all to see, after our local yards’ latest quarterly results, that the Oil and Gas industry remains in a trough, one where we are nowhere near the end of the tunnel to see a glimmer of light.

Just like the airline industry, the offshore industry is unlikely to witness a quick turnaround in today’s context, one where economic activities around the world have been severely curtailed due to COVID-19 which is still spreading like wild-fire. I have already given up tracking the daily cases happening around the world.

The oil market could be facing a new glut again as OPEC prepares to open the taps.

In short, I believed and I have mentioned this many times, that keeping status co will be detrimental to all stakeholders in this equation (Shareholders of Keppel, SCI, SMM, Temasek, employees, etc). If nothing is done by Temasek, we might not have any rig building yards by the end of next year.

Once the pride of Singapore, providing tens of thousands of employment opportunities (many of them foreign workers nonetheless), I don’t think these companies can continue to sustain such massive losses for long.

Hence, I believe that the ultimate consolidation between Keppel and SMM seems to be the only viable solution in the current context, one that is facilitated by Temasek.

The wildcard here is potentially the EGM between SCI and SMM shareholders which might throw the whole situation into disarray.

SMM minority shareholders can still reject the demerger deal, with the belief that the huge dilution is not in their best interest. In this case, Temasek might not be able to gain majority control over Sembcorp Marine and the purpose of owning majority ownership of Keppel might become pointless, in the sense that a quick facilitation of a merger between our two yards might no longer be feasible.

The pre-condition offer for Keppel might thus be Temasek’s insurance policy. In the event that the SCI-SMM demerger deal is not approved, then it might be pointless to have majority ownership of Keppel and Temasek can just trigger that clause and walk away from the deal. If the demerger deal is approved, they can choose to waive off the pre-conditions.

The EGM between SCI and SMM might be an interesting affair to watch, with many believe that it is already a shoo-in for the deal to go through. Is it?

This is just my own speculation here hence, do read it with a pinch of salt.

The share price of Keppel will likely fall on Monday, in my view and if the fall is large enough, it could be an opportunity to buy on weakness, holding the view that the restructuring deal between our local yards remains on the table.

Will the contrarian view of selling your “stable” bank shares and buying into Keppel be one that could possibly pay the dividends that you are thirsting for?

Not a recommendation over here but a food for thought. For disclosure purposes, I have got no stakes in our banks or Keppel at the current moment, preferring to watch the developments from the sidelines.

If you enjoyed reading this article and various other investment + personal finance articles, do visit New Academy of Finance. Royston has more than 10 years of buy and sell side experience as a financial analyst. He constantly posts interesting, valuable and actionable articles.

If you’d like to find out more about the TradersGPS system, click the banner below.