Financial Freedom Series: 7 Ways To Create Passive Income

On the subject of financial freedom, one of the first things that come to mind is undoubtedly passive income. This is because passive income is defined as income that requires little to no effort to earn and maintain.

Little to no effort to earn and maintain! That sounds like you’ll have the freedom of time to do a lot of other things which interest you. No more rat race, no feelings of being stuck in a place for the sake of money.

To arrive at that stage, we must first lay the groundwork…

Earlier in this series on the Road To Financial Freedom, I mentioned that our funds are like water. Think in terms of how we can have diverse sources in order to meet a growing demand. An important factor to note when it comes to wealth-building, is to start early. Don’t forget that your money is able to compound. Plus, on a more sober note, time is not on our side to begin with.

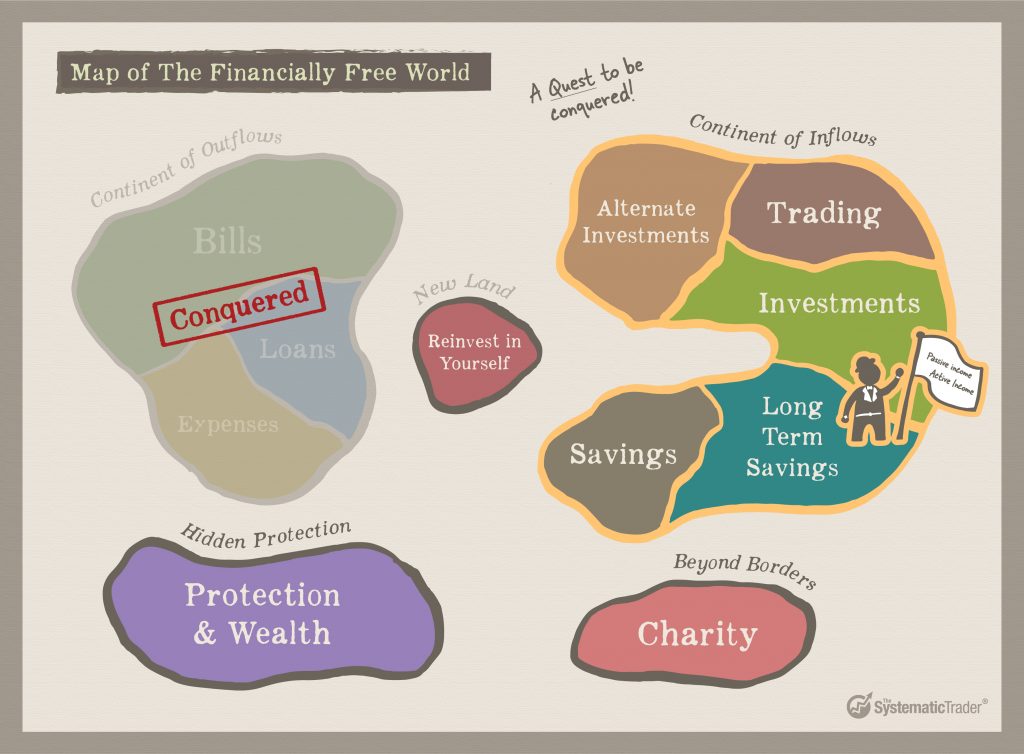

If you have joined the conquest of the Continent of Outflows and reduced your expenses, that only makes this Continent of Inflows much easier to conquer. The less you need to spend, the less you need to earn to achieve financial freedom.

You could be lacking in ideas as to how to diversify your sources of passive income. Or perhaps facing challenges when it comes to actual execution. Either way, this article explores some ways to help get you on track.

1. Investment: A Little Research Goes A Long Way

“Saving for a rainy day” was a piece of advice given from my parents. Growing up, I would diligently save as much money as I could. It paid for my school fees, funded overseas trips, and everything else in-between. Above all, it gave me the confidence that I was able to live within my means. All thanks to the consciousness that I always had money in the bank.

As I progressed into the working world, leaving my money in the bank increasingly seemed like a poor decision. The interest rates were low, and it didn’t seem like my money was working hard enough for me.

I learnt that investment, rather than savings, would be a better place for my wealth to grow.

Among the innumerable companies that are listed on the various stock exchanges, it could be daunting to know which to invest in. One of the common strategies is to invest blue-chip, dividend-yielding companies.

In Singapore’s context, banks and real estate investment trusts (REITs) are some of the popular choices for investors to gain dividends. You could also look up the rankings of the dividend companies at dividends.sg to help arrive at a decision. In the wider context of the US, there are also dividend aristocrats which have a track record of increasing dividend yields for minimally the last 25 consecutive years.

This is just thinking about the dividend yield from the stocks. We have yet to even consider capital gains!

Given that the stock market is up 70% of the time, even if you were not able to time your entry into the market, it is almost certain that your wealth would grow over time. The key is to select good companies to invest in so that they can put your money to good use.

This serves as a solemn reminder that the earlier you invest, the harder your money can work for you, not lose out on inflation, compound over the years, and become financially free. With little to no effort required over the years, it truly is passive income.

2. Savings: You Still Need Liquidity

After all that was said about leaving savings in the bank, it is nonetheless a crucial component of financial freedom. If all your funds were committed to the respective investment instruments, how would you be able to perform transactions and finance day-to-day expenses?

To sacrifice income for liquidity. That’s what it means to have savings in the bank.

Even so, having sufficient liquidity in your funds brings a sense of assurance. That’s why it is often recommended to have minimally 3-6 months’ worth of your monthly expenses in the bank. In the event that the rainy day does come, you wouldn’t be helpless in that situation and at least have the means to tide through.

Now that we’ve established that savings is essential, the next thing is to make sure you’ve got the most suitable type of savings account to maximize your interest rate, which serves as a form of passive income. In some ways, it’s similar and could even be linked to knowing what kind of credit card works best for you.

Based on your work status (e.g. salaried or freelance), spending habits and level of income, determine which bank’s savings account would yield the most realistic interest rates. Nowadays, there is no lack of research already done for you (https://blog.moneysmart.sg/savings-accounts/best-savings-accounts-singapore/). The bonus is that these articles are updated on a regular basis to reflect the changes in the interest rates. For instance, a recent update brought about by the economic impact of COVID-19.

3. Long-term Savings: Systematic Savings For A Defined Expense

While you keep savings in the bank to have liquid funds, long-term savings are entirely different. The goal is to save for larger, more defined expenses such as your retirement fund and children’s education. In fact, the instrument of choice is a little closer towards investments:

- Savings should be consistent and systematic (dollar-cost averaging)

- Low-cost, diversified, and compounds over the long-term

- Low-risk; instrument must not hit 0

- Returns should make better than inflation

Exchange-traded funds (ETFs) fulfill this set of criteria well. It could be an index fund such as the Straits Times Index (STI) in Singapore, or sector-specific ETFs such as iShares Global Clean Energy ETF (ICLN) in clean energy. The idea is to have a basket of companies so that there is still portfolio diversification, thereby reducing the overall risk exposure in the event of a downturn.

Then when the time is ripe, you would have the funds readily available. Plus, rather than the interest rates offered by banks in the case of typical savings, the returns from long-term savings should outweigh that of inflation.

4. Property: If You Have Higher Capital

If you had a choice, you would most certainly prefer to be a landlord rather than a tenant. We see it in movies and drama serials from time to time – being a landlord looks like the way to stable passive income.

When it comes to property investment though, it typically requires a high capital investment. Unless you have a six-figure sum available, venturing into properties could be a less viable strategy. Depending on your choice of residential or industrial property, there is also a list of considerations as to what makes a good property investment.

In order for you to collect rental from the property, you would first need a tenant. Yes, it means that you do need to put in a little work and capital for there to be passive income.

5. Affiliate Marketing: Some Work Involved

Property rental isn’t the only method which involves active work for passive income. Affiliate marketing, too, is another way which involves getting paid to drive customers to purchase goods and services. Unlike property rental, it is suitable for those who don’t have much capital to begin with. You could also think of it as one of the ways influencers can get an income.

While it is true that you have to put in the marketing effort for there to be sales, success does build up over time. Since the links and assets are available online, it is up to you to leverage on what you’ve done by driving traffic and exposure. Plus, it is entirely up to you to choose what to promote. If you’re going to recommend a product to your friends anyway, why not have them go through your affiliate link?

Some examples of affiliate marketing programmes include that of Amazon, Lazada and Qoo10. Tripadvisor would have made a fun choice as well, but let’s wait for inoculations to achieve more success and borders to gradually open.

6. Intellectual Property: Even More Work Involved

Yes, you could earn a passive income from royalties. Here, you’re putting your hours instead of your funds to work.

It means that you would create assets and be paid for others to use them. But well, if it’s a process you enjoy or if you’re already creating assets anyway, this may not be as difficult as it sounds.

Some examples of assets include designs, photos, music, writing, and even codes. Though the income might not be as consistent as you’d like, especially in the beginning, weigh your efforts against the goal of financial freedom. Remember that the first step to financial freedom is to trust the process and not give up.

7. Staking Cryptocurrency: If You’re Into Alternate Investments

Last but not least, is to foray into the newest topic among all – cryptocurrency.

Similar to the concept of collecting rental from property, it is also possible to collect a staking reward from your cryptocurrencies. However, to explain what staking is and how it works is beyond the scope of this article. For starters, this guide by Seedly provides a comprehensive overview on how to get into this newest form of passive income.

Plus, if you have your reservations about cryptocurrency, it serves as good reading too.

On that note, this sums up the 7 ways to generate passive income in 2021 and beyond. However, we are not quite done with the topic of cryptocurrency yet. In the conquest of the Continent of Inflows, we will continue to explore the area of Active Income. In terms of trading and alternate investments, it is no secret that cryptocurrency is one hot topic to look out for.

Stay tuned to the next parts of this series as we forge ahead into the terrains to be discovered and conquered, and focus on practical, actionable steps which you can take.

If you’d like to get a FREE e-course and learn how to better time your trade entries, click the banner below: