China Sunsine: The Sun Is Still Shining Brightly On This S-Chip

This is a very insightful fundamental view from our guest writer, of a rare S-chip, China Sunsine.

Fundamentals can paint a detailed picture of the business.

There is certainly something new to learn from the great analysis work by our guest writer, enjoy!

If fundamentals aren’t your style, check out how TradersGPS can help you,

China Sunsine’s Company Background

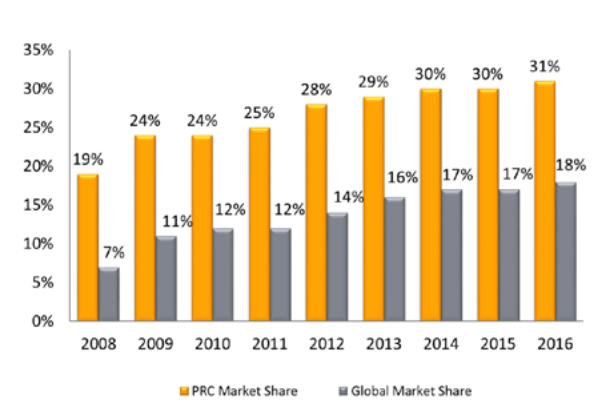

One might be surprise to find that we have got a locally listed S-Chip play that is a global market leader in its own rights. That company is none other than China Sunsine, the LARGEST rubber accelerator producer globally (with an 18% global market share) and the BIGGEST insoluble sulphur producer in the PRC.

The company boasts a strong clientele base that consists of the largest tire manufacturers in the world such as the likes of Bridgestone, Michelin and Goodyear etc (serve more than 65% of the TOP 75 global tire manufacturers), all market leaders in the realm of tire manufacturing.

China Sunsine has been listed on the SGX since 2007 and has since grown its capacity by leaps and bound. China counters have had the stigma of RED FLAGS and a NO GOs over the years.

However, we believe that China Sunsine’s longevity as a S-Chip on the SGX and its share price appreciation speaks volume of the credibility in its business model and not a “fly-by-night” scam waiting to erupt. Its latest SGX announcement will likely allay investors’ “S-chip” fears, in our view.

Institutional Funds Jumping On The Bandwagon

The company on 10 May announced in a press release that it has sold 27.6m treasury shares that were accumulated at a cost of SGD0.233/share (refer to AR2016 note 20b), or total cost of SGD6.4m, at a price of SGD0.646 which will yield a net return of approx. SGD17.5m or net profit of SGD11.1m which could be recognize as a one-off gain.

These treasury shares were sold to various institutional funds, which included Asdew Acquisitions, Island Asset Management and ICH Capital as well as corporate and individual investors.

This is a major positive in our view, given that it can be seen as a “stamp of approval” from these funds of the legit nature of this particular S-Chip counter, as well as their confidence of its future growth potential.

While one might highlight the fact that these share placements were concluded at a 9-10% discount to the last traded price (and hence not a fair one to existing shareholders) and that there was no moratorium that forbids these funds to immediately flip for a profit, we believe that this is likely the intention of the company to facilitate the sale of shares to allow more retail investors to partake and hence increase overall liquidity of the counter in due time.

We do not foresee these funds risking their reputations to generate the “meager” 9-10% return by fully exiting their positions immediately. Instead they are likely aligned with our view that China Sunsine presents strong growth potential that warrants a longer-term hold.

China Sunsine also highlighted that proceeds from the treasury share sales would be used to fund future dividend payments. A full single payout would yield 5% at current stock price level. More critically, that will signal management’s shareholder friendly attitude and provide a major confidence booster to existing and potential investors of China Sunsine.

1Q17: Not Just A One-trick Pony

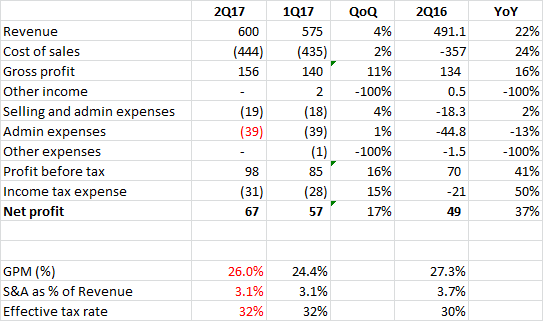

We believe a focus on the company’s fundamentals is likely as critical as events happening on its corporate front. The company registered a “phenomenal” (in management’s own words) 1Q17 that saw earnings increased by 70% despite only a 29% growth in top-line and gross margins maintaining at c.24%.

The key earnings booster: a 12% decline in administrative expenses.

According to management, the high administrative expenses incurred in 1Q16 (RMB44m) vs. 1Q17(RMB38.6m) was due to over accrual of headcount-related expenses in the previous year and that the current quarter expense figure is likely more of a normalized one.

Lets take a journey back to 2Q16 where administrative cost amounted to RMB44.8m. If we believe in management’s “guidance” of a normalize figure in 1Q17, then 2Q17 can also witness a potential expense savings of c.RMB5m vs. 2Q16 (10% benefit to bottom-line).

This is not the only operational improvement that excites us.

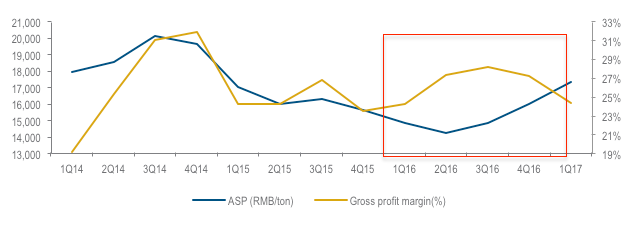

1Q17 is seasonally the weakest quarter in terms of production due to factory closures as a result of CNY. Margins were historically also lower in 1Q17 vs. 2/3/4Q.

We expect production levels to increase in 2Q17 vs. 1Q17.

Assuming constant ASP, that should result in higher revenue QoQ. 1Q17 generated RMB575m in top-line and we believe the company has got the potential to generate record revenue of RMB600m in 2Q17, the key reason being our observation that ASP of its key rubber accelerator product continues to be on an uptrend in Apr-YTD May 2017 vs. Jan-Mar 2017. We will provide an explanation on the strong ASP increment in our later section.

Assuming a same margin of 24.4% generated in 1Q17 for 2Q17, gross profit could hit RMB146m on the back of RMB600m in revenue, not overly exciting when compared to 1Q17 gross profit of RMB140m.

However, we do see strong reasons that margins will likely exceed 24.4% in 2Q17 and that is predominantly a result of slower raw material price growth vs. ASP growth, which again I will elaborate in the later section. Management guidance is that 1Q17 is usually a weaker quarter in terms of margins and we should expect improvement in the second quarter (due to removal of CNY effect).

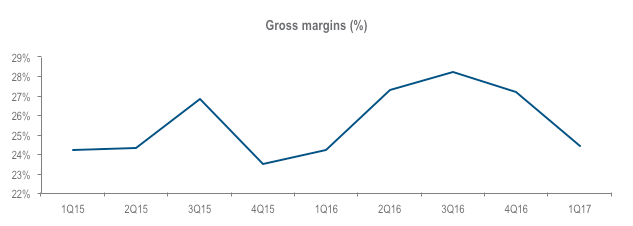

While the chart below does not show a strong seasonality correlation for the Group’s gross margin, we assume a higher gross margin of 26% in our forecast for 2Q17. Assuming stable administrative expenses, we could see 2Q17 net profit being at RMB67m (vs. RMB57m in 1Q17) on a conservative basis.

This compared to RMB49m generated in 2Q16 and we should expect at least a 37% YoY net profit growth as our “base case” scenario. On a “Worst case” scenario, a 20% net profit growth can be reasonably expected on a YoY basis.

2Q17 vs. 1Q17 P&L assumptions

The Devil Is In The Details

It is easy and sometime complacent to just assume that gross margins in 2Q17 will be stronger than 1Q17 based on management guidance. We however, have highlighted that we do not see a strong seasonality correlation.

Our deep-dive analysis has however ascertained that there is indeed a high probability that 2Q17 margins will be higher than that of 1Q17.

Key reason: ASP of rubber accelerators has increased (and still increasing) from 1Q levels while key raw material component (Aniline) has remained largely constant (in-line with crude oil prices).

While both components (ASP and Raw materials) tend to trend in line, the recent displacement in directional movement between the two could signal a strong margin improvement potential for China Sunsine ahead.

While ASP continued to decline and hit a bottom in 2Q16, GPM improved as a result of raw material prices falling faster than ASP decline in 1H16. However, that trend reversed in 2H16 on the back of stronger crude prices.

ASP has been appreciating since bottoming in 2Q16 as a result of an industry-wide supply curb where the government has been particularly strict in closing small-mid size factories that have been constantly flouting environmental rules (given that this industry is rather pollutive by nature).

China Sunsine, which has been investing in environmental protection measures (approx. RMB60-70m per annum) is likely to be the key beneficiary in this industry-wide supply clampdown, which has affected overall supply amid strong product demand.

Hence, due to lower product availability, existing incumbents (bigger plant players) benefit from both higher selling prices of their products in addition to likely gaining a larger market share.

Sunsine COGS

1Q16-2Q16: crude price weakness with Brent hitting USD30/bbl. This resulted in cost rising at a slower pace than ave selling prices in general and result in higher GPM

3Q16-1Q17: crude prices increasing from USD30/bbl level and stabilizes at approx. USD50/bbl. Cost increasing much faster than ASP. This resulted in declining GPM

2Q17E: ASP continues to climb by 15% due to supply constraint while cost has stabilized at near the same level of 1Q17.

Raw material cost (mainly aniline) is pegged to the cost of crude. In a normal circumstance, the cost of raw material would dictate the selling prices of the product. However, due to the current supply-demand imbalance, despite raw material cost holding steady from 1Q17 levels, ASP as highlighted have increased by approx. 15% (source) which will have a direct flow-though impact to gross margins (a potential 5ppt improvement in gross margins to 29% in either 2Q17 or 3Q17).

This is the exact scenario that happened in mid 2014 whereby the government clamp down actions on small producers have resulted in product ASP increase (that subsequently proved to be unsustainable) in addition to the collapse in crude prices that saw margins ballooning in excess of 30% in 3Q/4Q14.

Can History Repeat Itself?

This is likely the question in savvy investors’ mind. Is the current rise in ASP and fall in raw material cost resulting in higher margins sustainable in the longer run? While we do not have a crystal ball, at least for the next couple of quarters, we do not expect the government to relent on their efforts to further improve the pollution issue in China, which means smaller players are not expected to return.

How about bigger boys expanding their capacities? Besides China Sunsine, there are likely 2 other major producers of rubber accelerator products: Yanggu Huatai and Kemai, the former being a listed entity on the shanghai stock exchange while the latter is a private company which has recently applied for an IPO that has not been approve due to violation of certain safety and environmental rules according to our knowledge.

Both entities are not comparable to China Sunsine in terms of financial health, with China Sunsine being free of debt and can sufficiently generate operating cash flow to fund its capex commitment.

Yanggu Huatai had the intention to do a share placement but that was not approved by the authorities due to the significantly dilutive impact on existing shareholders.

Kemai, pending an IPO, likely also lacks the necessary capital to embark on a large scale expansion. This will result in a scenario where supply is likely being restricted as both small and large players (with the exception of China Sunsine) have difficulties in expanding their capacities aggressively.

What Happens Next?

While we are relatively confident that the company will demonstrate decent YoY growth in 2Q17 as highlighted by our analysis above, what happens beyond the next quarter? China Sunsine has already set aside approx. RMB250m (key capex being the 10,000 ton TBBS plant, highest margin accelerator with strong demand currently) for capacity expansion, which will be completed in 2H17, with full deployment likely in beg-2018.

We can hence expect continual growth in 2018 vs. 2017 on the back of the company’s capacity expansion plans. The company can further scale up its TBBS expansion by an additional 20,000 tons for 2019 at a marginal cost of RMB100m (most of the infrastructure already in place).

Re-Rating In The Offing?

With its market leading position, China Sunsine should see a re-rating on its business, particularly with such strong earnings growth potential.

Despite market skeptics that the company will not be able to generate growth anywhere close to the “phenomenal” 70% rate that it recorded in 1Q17 (due more to a low base year in 1Q16).

iIn 2Q17, we will not be entirely surprise if the company can maintain such outperformance in the coming quarters (particularly in 2Q17 as production growth is still feasible on a YoY basis whereas the company will not be able to generate significant YoY volume growth in 3Q17 due to the high volume base in 3Q16 and current capacity bottleneck, new capacity to enter mostly in 4Q17 and 2018).

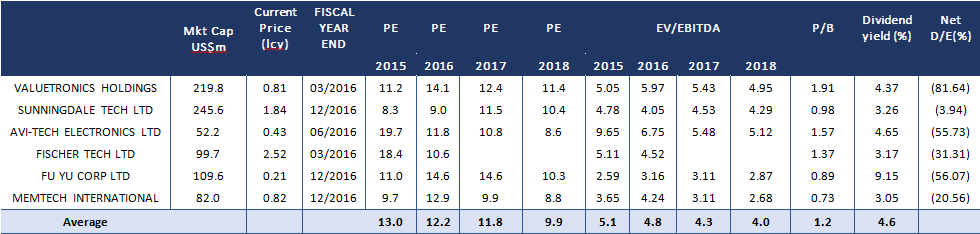

On our estimates, the company is currently trading at a forward PER of 5.5x vs. industrial peers (currently whats hot in the Singapore market) at an average of 11.8x. EV/EBITDA is approx. 3x vs. peers 4.3x.

Assuming a target forward PER of 8x as a fair value, due to its status as an “S-Chip” despite strong growth potential, we derived an estimated fair value of approx. SGD1.00.

China Sunsine is looking attractive in all areas vs. industrial peers, which include growth prospects and valuations on forward PER or forward EV/EBITDA basis. It is comparable on a forward PBR but pays a lower dividend yield of c.2% vs. peers’ average of 4.6%. However that could change in the coming quarters with the recently sold treasury shares (potential bumper special) as well as strong operating cash generation with no more debt repayment commitments.

I hope you found this piece as enlightening as I have.

To find out more about TradersGPS and how it can make a huge change to your trading returns,

Good trading folks!