5 Best Blue Chip Growth Stocks To Buy Now

In this article, we will be highlighting 5 companies that have been able to consistently generate 10 years of earnings growth. According to the Stock Rover screener, there are only 16 companies in the entire S&P 500 index that has achieved 10 years of consecutive earnings growth.

This is no easy feat. But what is even more difficult to achieve is to consistently outperform the stock market over the past decade.

Out of the 16 companies that have achieved consecutive earnings growth, only 5 have seen their share prices consistently beating the S&P 500 index over these horizons: YTD, 1-year, 2-year, 3-year, 5-year, 10-year.

Which are the 5 blue chip growth stocks and what common characteristics do they hold that allow them to achieve such a feat?

#1: T. Rowe Price Group (TROW)

This is a company that provides asset management services for individual and institutional investors. It offers a broad range of no-load US and international stock, hybrid, bond, and money market funds. At the end of 2020, the firm had close to $1.5trn in managed assets, composed of predominantly equity (61%), balanced (28%) and fixed-income (11%) offerings.

Approx 2/3 of the company’s managed assets are held in retirement-based accounts which provides T- Rowe Price with a somewhat stickier client base than most of its peers.

Why Is TROW The Best Growth Stock?

The asset manager has a few key competitive advantages that investors should know about:

T. Rowe Price is an active manager, although back in Aug 2020, the Group ventured into the ETF space by launching 4 new ETFs: the Blue Chip Growth, Dividend Growth, Equity Income, and Growth Stock ETFs.

As an active manager, the Group also has a fantastic track record of beating both its peers as well as the indexes. Its active management prowess should lead to more inflows and revenue in 2021. Already, its 1Q21 revenue is up a solid 25% on a YoY basis and that should set it on course to yet another record-breaking year in terms of top-line performance.

The Group has a pristine balance sheet, with almost no long-term debt and has $2.8bn in cash and cash equivalents as of 1Q21. Its great balance sheet has enabled the company to maintain its status as a Dividend Aristocrat, with 35 years of consecutive dividend increase.

Coming back to its financials, the chart below shows both the revenue and EPS growth of the company.

The company has seen its revenue growing from $2.7bn in 2011 to $6.2bn in 2020, a CAGR of approx 9.5% during this period. Its EPS has grown from $2.92 in 2011 to $9.98 in 2020, a CAGR of approx 14.6%, a much faster growth as a result of share buybacks where the company uses its strong free cash flow generation to consistently buyback its shares (2011: 294m, 2020: 231m). Consequently, TROW was able to grow its EPS at a much faster clip, music to the ears of shareholders.

So while there might be uncertainty ahead, this is one company that will deliver both income and equity through the ups and downs.

The company is one of those rare gems that have been able to consistently outperform the S&P 500 over a 10-year horizon, generating total returns of 367% vs. the S&P500 returns of 303% during this period.

On a YTD basis, TROW generated returns of 34%, substantially outperforming that of the S&P 500.

For those looking to partake in an asset management company, there is no better company than T. Rowe Price to get you started.

Now taking a quick look at its chart on TradersGPS over the past year, TROW has been on a steady ascent since the entry signal in December 2020. With an entry at approximately $140/share, you would be up 50% in this counter at its current share price of $211.10.

#2: IDEXX Laboratories (IDXX)

IDEXX laboratories primarily develop, manufacture, and distribute diagnostic products, equipment, and services for pets and livestock. Its key product lines include single-use canine and feline test kits that veterinarians can employ in the office, benchtop chemistry and hematology analyzers for test-panel analysis on-site, reference lab services, and tests to detect and manage disease in livestock.

Essentially, IDEXX offers an all-in-one suite of products that handle everything from workflow management to blood and chemistry analyzers, even offering outside reference labs for smaller practices that wish to get accurate and timely results in 2 days or less.

IDEXX makes money when pet owners visit their veterinarians and run diagnostic tests. COVID-19 initially hurt its business, where the onset of the pandemic had people running scared to bring their pets in for treatment. But initiatives taken subsequently such as curbside pet drop-off made the visits safer.

Surprisingly, COVID-19 didn’t derail its business growth and the company was able to grow its revenue by 12.5% on a YoY basis to $2.7bn. EPS grew by an even stronger 37% YoY to hit a record high of $6.71. The stronger EPS growth vs. top-line growth was due to stronger cost control as well as share buyback efforts made by the company.

From 2011 to 2020, the company grew its revenue from $1.2bn to 2.7bn or a CAGR of 9.3%. EPS grew from $1.39 to $6.71, a more impressive 19% CAGR. At the same time, its outstanding shares declined from 116m to 87m.

IDEXX, unlike TROW, is not a dividend payer, focusing on reinvesting its free cash flow back into its business. However, I will not be too surprised to see IDEXX paying shareholders a dividend in the coming 2-3 years as the requirement for capital to fund capital expenditure tails off.

In the coming year, IDEXX had a good headstart with its revenue increasing from $626m in 1Q20 to $778m in 1Q21, led by higher growth in diagnostic recurring revenue. Another area to look forward to is the launch of Procyte One, IDEXX’s new best-in-class hematology analyzer. The company has priced the machine attractively to encourage greater adoption and expects to sell over 100,000 units in its first year.

The company has done a good job in the US and still has plenty of untapped growth potential domestically. It is, however, its international growth, where the company now accounts for more than 30% of its top-line which could further hyper-charge its growth in the coming decade.

As can be seen from the table below, this is one company that has achieved tremendous outperformance over the past 10-years vs. the S&P 500, outperforming the market by an incredible 1240% during this period.

This is no meme stock but a consistent price outperformer with earnings to back it up. Its share price have outperformed my expectations in 2019 and 2020.

IDEXX is also one of the 8 outperforming stocks I highlighted back in May 2020 at New Academy of Finance which investors should consider getting into.

This is one pet stock that is treating its shareholders well and should continue to maintain its outperformance vs. the market in the coming decade.

IDEXX has had entry signals as recent as end May 2021. Entering this stock at $559 would have seen this counter gaining $100 over the past month. For those looking to scale-in their positions into IDEXX, it remains to be seen if there would still have opportunities in the near future as the bullish momentum continues.

#3: Pool (POOL)

Pool is a consumer cyclical stock that distributes swimming pool supplies and related products. A very simple business model that sells national-brand and private-label products to approx. 120,000 customers. The products include non-discretionary pool maintenance products like chemicals and replacement parts as well as pool equipment like packaged pools (kits to build swimming pools), cleaners, filters, heaters, pumps, and lights.

The company’s main target consumers are pool builders and remodelers, independent retail stores, and pool repair and service companies.

COVID-19 has been a boon for the company as stay-at-home measures and social distancing have encouraged a boom in discretionary spending on the home and garden segment. Naturally, investors are concerned that the strong growth seen in 2020 will fade away in 2021 as reopening takes leg.

However, the company reported a torrid 57% YoY revenue growth in 1Q21 even as the pandemic recedes in the US, which management believes that the trend of work-from-home is here to stay. This is one “work-from-home” company that is likely under-mentioned by the street.

As can be seen from the chart below, the company managed to grow its revenue from $1.8bn in 2011 to $3.9bn in 2020, a CAGR of 9%, similar to IDEXX. Again, its EPS grew by a more impressive CAGR of 22% during this period, increasing from $1.47 in 2011 to $8.97 in 2020, boosted by strong operational cost control as well as a reduction in outstanding share base.

During this period, its net profit margin has improved every single year from 4% in 2011 to 9.3% in 2020 which highlights a certain level of operating leverage.

The street expects the company to generate $12.41 in EPS for 2021, which is a strong 38% YoY growth vs. 2020. This growth however is expected to moderate to a 7% increment in 2022.

Similar to IDEXX, POOL has strongly outperformed the S&P 500 over the past decade. This is one company that is operating a very simple business model with no rocket science R&D required and yet it can consistently outperform the market which makes its success all the more intriguing.

This is one stock that I will like to “dig into” and find out its secret sauce as to why the company can be so profitable despite running a pretty simple business model, one which doesn’t seem to have much of a barrier to entry.

According to TradersGPS, POOL has had several entry signals this past month as well. Entering this counter at $461 in late June would give you a modest return of 3% to date over 3 weeks. Bullish momentum on POOL appears strong as well. Once again, those looking to scale-in positions might want to keep a watch on this counter.

#4: Mettler-Toledo Intl (MTD)

Mettler Toledo Intl or MTD operates in the healthcare industry and supplies weighing and precision instruments to customers in the life sciences, industrial, and food retail industries. Its products include laboratory and retail scales, pipettes, pH meters, thermal analysis equipment, metal detectors, and Z-ray analyzers.

The company is the market leader for weighing instrumentation and controls more than 50% of the market for lab balances. Unlike both IDEXX and POOL which are predominantly US-centric, the business for MTD is geographically diversified with sales distribution roughly as follows: the US at 30%, Europe at 30%, China at 20%, and the Rest of the World at 20%.

Now, MTD is a stock that will not be on everyone’s radar. I reckon that most investors out there will not be familiar with this counter which boasts a market cap of $32bn. It is also not a stock that is widely covered by the street, with just 7 houses covering the counter and the majority of them have got a HOLD/SELL rating on the counter.

Nonetheless, this is one stock which you should be keeping a closer watch, as seen from the chart below, where the counter has been a steady performer in terms of both top and bottom-line.

The company grew its revenue from $2.3bn in 2011 to $3.1bn in 2020, or a CAGR of 3.3%, not as impressive compared to our stocks in this list. What is more impressive is the growth in its EPS, from $8.21 in 2011 to $24.91 in 2020, a CAGR of 13.1%. Again, this is a result of operational efficiency as well as a reduction in its outstanding share base, from 33m shares to 24m shares during this period.

What I like about this company is that it does not need to spend a huge amount of CAPEX to grow its business. Its annual CAPEX amount has declined from $98m in 2011 to $92m in 2020 when its operating cash flow ballooned from $281m to $725m over the same period.

This translates to a substantial amount of free cash flow that the company “returned” to investors in the form of share buybacks.

Throughout the last 10-years, this unknown healthcare stock has consistently outperformed the S&P 500, as evident from the chart below.

While I will not be in a hurry to add on to this counter, considering the spike in its P/E multiple from an average of 35x to the current level of 50x, this is one counter that is on my watchlist to buy on the dips.

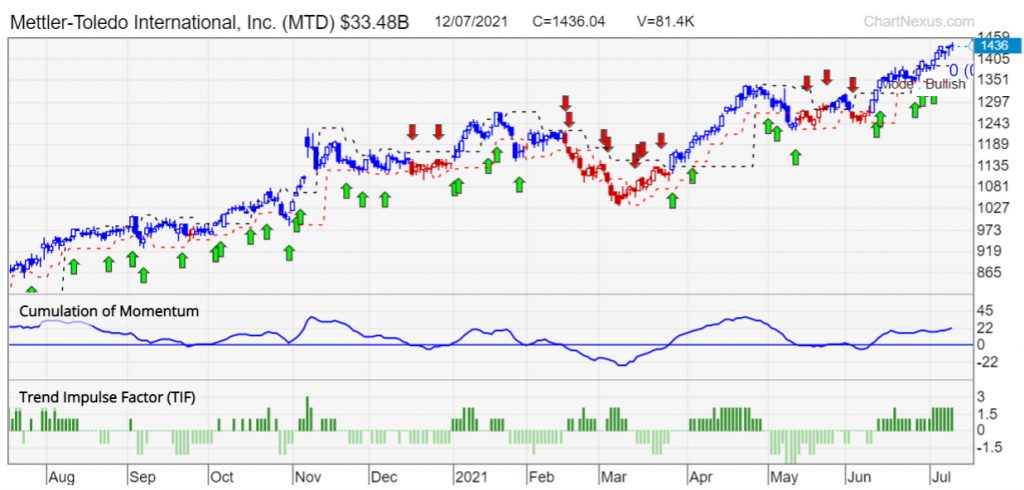

Bullish momentum for MTD has been strong over the past month as well. A recent entry identified by TradersGPS at $1352 would have reaped 6% gains over a one-month period. As with the other counters above, let’s keep a lookout on how this counter continues to perform.

#5: United Health Group (UNH)

United Health Group or UNH for short is the largest private health insurance provider in the US, providing medical benefits to 48m members across its US and international businesses at the end of 2020.

As a leader in employer-sponsored, self-directed, and government-backed insurance plans, UNH has obtained massive scale in managed care.

Along with its insurance assets, UNH’s continued investments in its Optum franchises have created a healthcare services colossus that spans everything from medical and pharmaceutical benefits to providing outpatient care and analytics to both affiliated and third-party customers.

The company presents a wide moat for investors looking for safe and strong businesses to hold through booms and busts. In 2019, UNH was the market leader in the US health insurance space, with a 14.1% market share, followed by Anthem (9.6%), Humana (8.4%), and Centene (8.3%)

Over the past 10 years, if you have invested in the company from June 2011 and held till today, you would have generated 819% returns on a dividend-adjusted basis. That crushes the S&P500 return of about 304% during the same period.

This is supported by its financials, with the company growing its revenue from $101bn in 2011 to $240bn in 2020, a CAGR of 10.8%. EPS grew from $4.73 to $16.03 in the same period, a CAGR of 13%. The stability in its financials is a pretty credible feat for a healthcare insurance company.

The company uses its strong free cash flow generation, which grew from $5.9bn in 2011 to $20bn in 2020 to buy back shares as well as pay shareholders a dividend, one which grew from $0.61/share in 2011 to $4.83/share in 2020.

Considering that the company’s payout ratio is just about 25-30%, there is plenty of scope for the company to continue growing its dividend payments in the coming years, with its consecutive dividend growth track record currently at 11 years.

While its outperformance vs. the S&P 500 is not as impressive as the other candidates on this list, this is one blue-chip dividend growth payer that can continue to reward shareholders in the coming decades.

I like the company at present because the valuation re-rating for the counter has not been as significant as the other candidates on this list, with the counter currently trading at approx 22x historical P/E vs. its 10-years average of 18x.

Last but not least, taking a look at UNH’s chart on TradersGPS:

TradersGPS has identified entry signals last week for UNH. While the counter appears to be trending sideways at the moment, it may still be a good idea to keep UNH on the watchlist.

Conclusion: Best Growth Stocks In The US To Buy Now

These 5 stocks have demonstrated stability in terms of earnings growth, with 10 consecutive years of EPS growth. Additionally, they have also shown that they can outperform the market consistently in terms of share price performances.

A few common characteristics among these companies:

- Their business has a moat which is evident in consistent revenue growth.

- They can achieve operating leverage where margins continue to improve as they grow their revenue. This translates to stronger earnings growth.

- They generate strong free cash flow.

- They use their strong free cash flow generation to buy back shares as an indirect form of returning capital to shareholders.

- They have high ROIC.

I believe that these 5 counters are all very decent candidates to buy and keep in one’s long-term portfolio and the probability of them outperforming the market over the next decade is more than ever, in my view.

However, I would like to point to my readers’ attention that many of these counters that have demonstrated earnings resilience even during COVID-19 have witnessed a huge re-rating in their valuation, in terms of P/E ratio.

Only 2 out of the 5 stocks in this list did not see a substantial re-rating in their P/E multiple: T. Rowe Price Group (17x P/E) and UNH (22x P/E).

Once again, this is not a recommendation to BUY or SELL these best blue chip growth stocks. Readers should do their necessary due diligence and evaluate if these stocks are suitable for their investment portfolio.

If you enjoyed reading this article and various other investment + personal finance articles, do visit New Academy of Finance. Royston has more than 10 years of buy and sell side experience as a financial analyst. He constantly posts interesting, valuable and actionable articles.

If you’d like to learn more about systematic trading to better time your trade entries, click the banner below:

One Response